Top five charts of the week

12 Mar

The top 5 charts of the week are chosen by our guest blogger Mihály Tatár and cover the recent jump in Italian long-term bond yields, the Trump effect in Central and Eastern European yields, the critical and worsening situation in Turkey, why we call copper “dr Copper” and why Facebook equity price downturns signal a big trouble… Click on the graphs to make them bigger.

1. Italy 10Y bond yield

- While the market likes the pre-election noises coming out of France (Macron looking competent and the refugee situation is contained), Italy remains a wildcard and the Italian 10Y yield doubled from 1% to 2.2%.

- Currently about half of the Italian parties are hostile to the Euro (Five Star Movement, Northern Leage, not to mention the topplied-by-Brussels Silvio Berlusconi), and Italy, with it’s large debt, failing banks and the still ’too strong Lira’ has good reasons to leave, or at least threaten to leave.

- The problem with Italy is that even with the most europhile leadership, it can be hit by one crisis after another. At an EURUSD of 1.05, and at a 10Y yield of 1%, it’s growth was a mere 0.9% in 2016, with Monte Paschi, the world’s oldest bank, collapsing. In ’normal times’, meaning without ECB intervention, the Italian 10Y yield used to be 4-5% – levels that the government couldn’t afford today.

2. Regional yields (Rephun 2021 USD, Poland 2021 USD)

- Regional USD bond yields have been in a steady downtrend – meaning cheap and stress-free financing for regional governments and companies – since the ECB monetary easing. (The easing targeted Euro bonds, but investors had no other alternative than to buy Dollar securities to reach serious yields).

- The Trump victory in November convinced the market that the trend is now turning (more spending, more growth, more inflation in the US), and yields jumped. In the case of Poland (rated A-), this meant a 70 basis points move. In absolute terms, this doesn’t look much – until one realizes that the ECB programme is soon over, and the Fed started an aggressive rate hike cycle in December.

- With the sound economic background of the region, a slow and gradual re-pricing is to be expected, but the times of cheap and easy money in USD are over.

3. The Turkish Lira

- At the moment of out the media focus, but the tanking of the Turkish economy continues. Inflation rose to almost 10% and unemployment jumped to 12% (from 8% in 2012), while GDP contracted almost 2% in the third quarter (Y/Y). The main pressure is on the Turkish Lira, which lost more than 60% since 2015 against the Dollar.

- Turkey and especially Turkish companies and households are over-indebted in Dollars, meaning any rise in USD rates puts more pressure on the Turkish economy. Without external help, Turkey looks like the perfect victim of the Fed rate cycle. For hedge funds, the question is whether the country will be allowed to fail: We are talking about the financial, commerce and pipeline hub of the region, not to mention the second largest NATO army and the refugee-keeper of the EU.

- On the other hand, the Erdogan regime has fewer and fewer friends by the hour, and even the rich Gulf states – old time sponsors – are frustrated with its reckless actions in Syria.

4. Dr.Copper

- Because Copper is important in almost all sectors of the economy (housing, factories, power generation and transmission, electronics), and can show economic expectations very clearly, it is dubbed as ’Dr.Copper’ by the market.

- After the 2015 panic about the impeding China collapse, Copper prices stabilized in most of 2016, and jumped after the Trump victory. The market expects massive spending projects from Trump, and traders now look frustrated that nothing happened so far, hence the slide in the last few days.

- It’s worth mentioning that Copper is also often used as hedge against inflation – after the Financial Crisis Fed programme, for example, it rallied more than 200% on the expectation that the Fed will cause a large wave of inflation (which proved to be delusional).

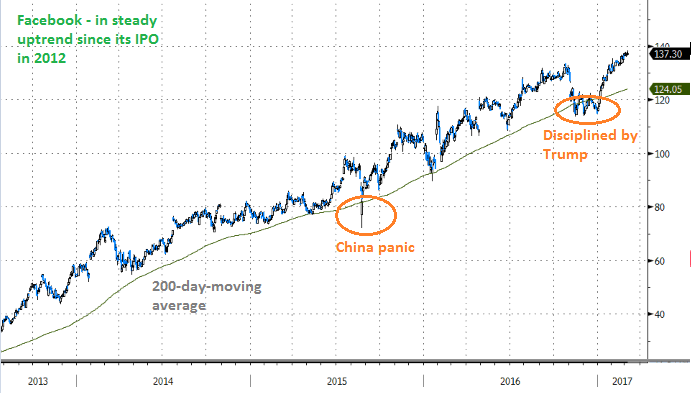

5. Facebook

- This chart is not here because anything happened to it, but because of its systemic importance. Facebook is the ’face’ of the US equity rally, rising 200% since it’s IPO in 2012. Every player has its stocks in their portfolio – private investors, pension funds, sovereign funds, hedge funds, central banks – meaning any large move here is quite telling.

- Facebook only had two serious downturns so far – the 2015 panic of China collapsing and the Trump victory (the company was effectively campaigning for Hillary Clinton).

If you liked the post, follow Barrelperday on Facebook!

Or subscribe to our Twitter feed or Newsletter

No comments yet